I am SO excited to share the newest Erin Condren products with you all! I'm going to show you some of their latest accessories and then flip through the LONG-awaited, much anticipated MONTHLY … [Read more...]

I picked my New Year’s Resolution!

I did it! It's February 15, and I finally picked my New Year's Resolution (yes, only one). I've never felt better about a resolution. You may recall my recent post about feeling overwhelmed by … [Read more...]

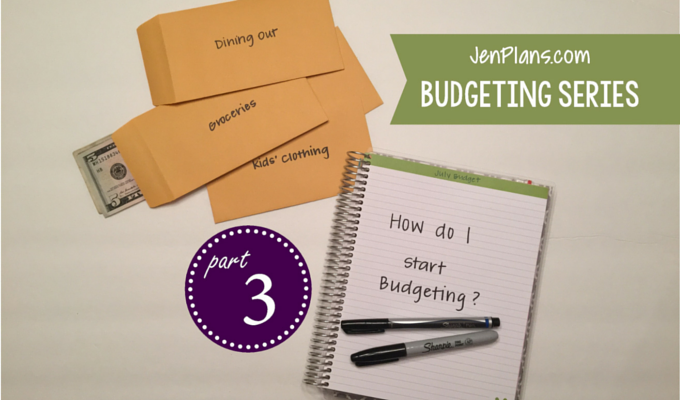

JenPlans.com Budgeting Series – Part Three

Welcome to the main event! It's time to MAKE A BUDGET! If you are just starting, you'll need to complete Part One and Part Two before moving on to this portion. Gather your information □ … [Read more...]

JenPlans.com Budgeting Series – Part Two

Welcome back! If you are checking in for part two in the budgeting series, read on! If you haven't seen part one yet, start here! Part Two is all about knowing your numbers. To properly build a … [Read more...]

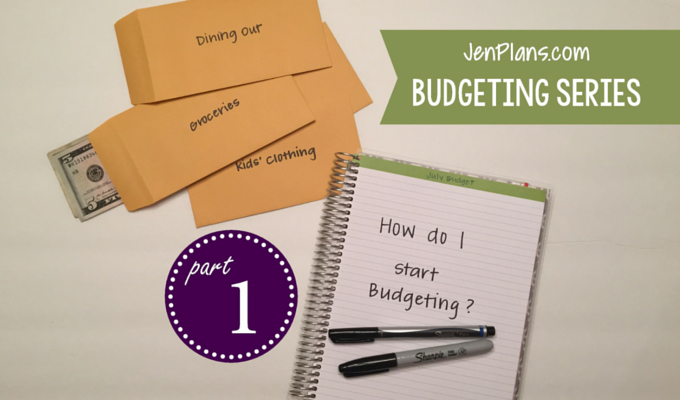

JenPlans.com Budgeting Series – Part One

DO YOU NEED HELP MAKING A BUDGET? Join me in this JenPlans.com Budgeting Series to gain control of your finances! I’ve done this series in a few private Facebook groups but I wanted to put … [Read more...]

Money and shame

Money shame is real. I had outlined this post when a dear friend sent me a text message. “Why do we go to the doctor when we’re sick, bring our car to the mechanic but we aren’t supposed to talk … [Read more...]