Welcome to the main event! It’s time to MAKE A BUDGET! If you are just starting, you’ll need to complete Part One and Part Two before moving on to this portion.

Gather your information

□ Categories (This comes from your 12-Month Spending History you completed)

□ Known Expenses (bills, debt payments, etc)

□ Known Income (if this is variable, you’ll use the variable income budget template linked below)

□ Way to keep track of budget (excel spreadsheet, pen and paper, etc)

Pick your format

□ If you have a FIXED (or mostly fixed) income, use THIS BUDGETING FORM.

□ If you have VARIABLE income, use the form above, AND THEN THIS.

Customize AND BUILD YOUR BUDGET!

□ Cross-check your categories with the ones on the budget form and add the ones you have that don’t appear on the forms.

□ Follow the prompts on each form and start filling in your KNOWN expenses first, then plan out what you’ll budget for the rest.

Don’t get discouraged!

It usually takes at least 2-3 rounds of this process while you figure out what numbers work

and what you need to adjust before they all balance out.

This is a learning process and even if it’s frustrating,

YOU ARE NOW IN CONTROL OF YOUR MONEY! And that’s SO EXCITING!

□ Sinking Funds! When filling in your sinking funds, you’ll divide out your expense by the number of months until its due if it has a timeframe (for example, if your $120 car registration is due next August, you’ll divide that category by 12 and then save $10 into that “sinking fund” each month. Come August, you’ll have all $120 saved, will withdraw it to pay the fee and will start all over again. If that registration is due in February, you’ll need to amortize that money over six months instead of twelve, so you’ll save $20 each month until February, THEN reduce to $10/month from then on out). If it DOESN’T have a timeframe (furniture replacement, car repair, etc), figure out how much you’d like to have saved based on your spending over the last 12 months and turn that into a monthly expense.

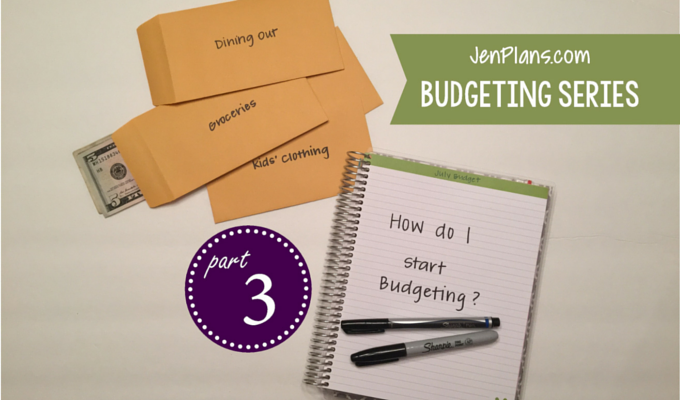

□ Be sure to note which categories have a little envelope designation next to it to show you which categories are recommended to be CASH categories. This will prevent over-spending. You can’t spend it if you don’t have it! You can use regular envelopes or make yourself fun fancy envelopes but you just withdraw the amount, stick it in the envelope and then carry the ones you need for that day. If you’re already using cash, GREAT! If you’re not, now’s the time to try.

□ Make your plan. When will you withdraw cash? When will you sit down to pay bills? Schedule your weekly reviews of all of your accounts and envelopes to see how everything’s going and to tweak where necessary.

If you think this is a bunch of bologna, TRY IT.

There’s no harm in trying something new. I challenge you to try it for one month –

it doesn’t have to be a lifetime commitment – just give it a shot for one month.

It will be a learning tool to teach you what you like, don’t like and how it affects your spending.

It is so important to learn about yourself in this process.

YOU’RE READY TO START! Happy Budgeting!

Jen, Thank you so much for your break out of how you made your budget. I read Total Money Makeover and when I got to the end I was like “this is great, but how do I REALY start”! I could get on board with the emergency savings fund and the debt snowball, but I thought I knew how to make a budget…obviously not if I’m in need of a total money makeover! This was super helpful and eye opening! Thank you!

Where Did You Buy The Envelopes You Use To Separate Your Cash ?

I just got them via amazon.com! Thanks!