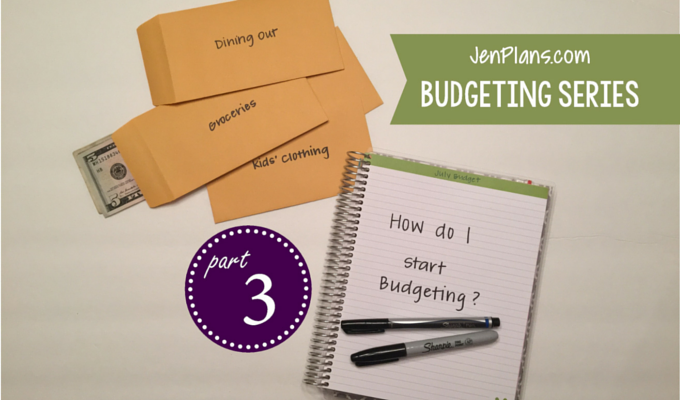

Welcome to the main event! It's time to MAKE A BUDGET! If you are just starting, you'll need to complete Part One and Part Two before moving on to this portion. Gather your information □ … [Read more...]

JenPlans.com Budgeting Series – Part Two

Welcome back! If you are checking in for part two in the budgeting series, read on! If you haven't seen part one yet, start here! Part Two is all about knowing your numbers. To properly build a … [Read more...]

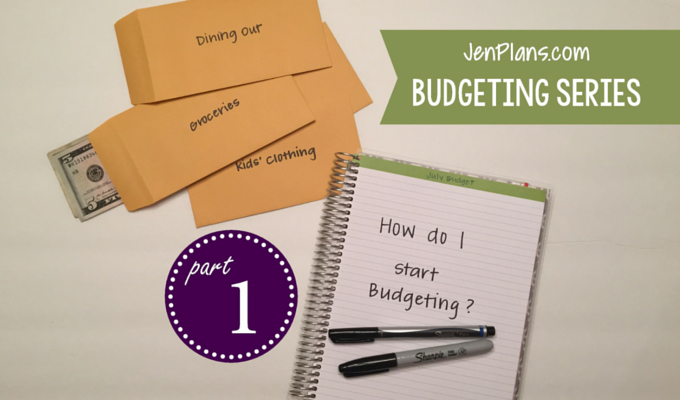

JenPlans.com Budgeting Series – Part One

DO YOU NEED HELP MAKING A BUDGET? Join me in this JenPlans.com Budgeting Series to gain control of your finances! I’ve done this series in a few private Facebook groups but I wanted to put … [Read more...]