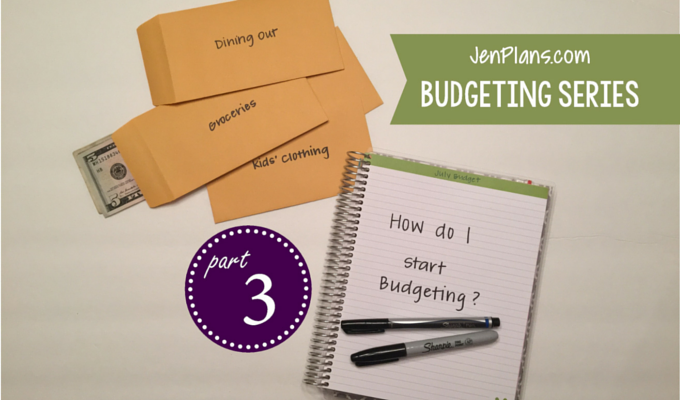

Welcome to the main event! It's time to MAKE A BUDGET! If you are just starting, you'll need to complete Part One and Part Two before moving on to this portion. Gather your information □ … [Read more...]

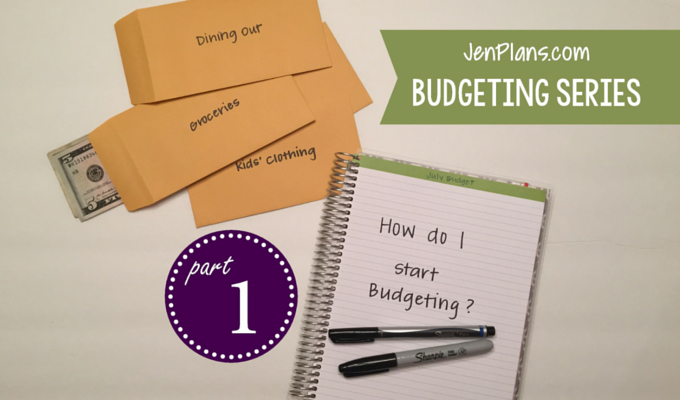

JenPlans.com Budgeting Series – Part One

DO YOU NEED HELP MAKING A BUDGET? Join me in this JenPlans.com Budgeting Series to gain control of your finances! I’ve done this series in a few private Facebook groups but I wanted to put … [Read more...]